August was an eventful month for investors. A US growth scare sparked an initial selloff, but markets quickly recovered as stronger economic data soothed recession concerns.

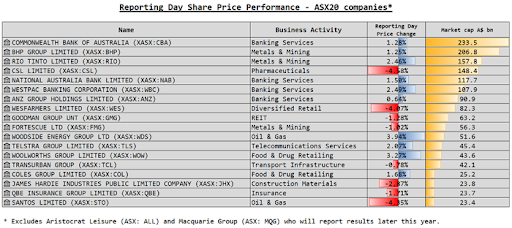

Most of Australia’s leading companies reported profit results in August and provided outlook guidance.

The profit season highlighted the disconnect between rising Australian share prices and softening earnings.

Aggregate ASX200 profits declined marginally for a second consecutive year amid subdued consumer spending, higher costs and weaker commodity prices. Against this backdrop, the ASX200’s +15% return over the past 12 months seems misplaced.

Individual company results and share price reactions were mixed, as shown in the table below.

The message on consumer spending was soft, with sales generally down. Well-known retail names including JB HiFi, Woolworths and Coles, have navigated this period well, managing cost pressures across their businesses.

Companies including AGL Energy, Origin Energy, Telstra and Transurban noted higher demand for hardship support due to cost-of-living pressures.

Higher listings at CAR Group (owner of CarSales) and REA Group (owner of realestate.com.au) are another sign of consumer stress, indicating a level of forced sales.

Seek described a weakening jobs market as more people seek work despite fewer job ads.

Various industrial and building materials companies noted subdued conditions in the housing sector. James Hardie reported a reduction in Asia Pacific Fiber Cement volumes driven by “weak demand in Australia”. Plumbing supplier Reece noted it is enduring a “softening housing market” that is “expected to remain soft”. Wesfarmers added that Bunnings sales have moderated in the first six weeks of the new financial year due to “continued market

-wide softening in building activity”.

Big bank results were respectable and generally well-received by the market as net interest margins stabilised. CBA reported that 90-day mortgage arrears had risen in line with historical averages. NAB noted “higher arrears for the Australian mortgage portfolio” and said business borrowers also feel stressed with “a continued broad-based deterioration in the Business & Private Banking business lending portfolio”.

Rising debt costs hit rail freight operator Aurizon and property groups Dexus and GPT as Australian interest rates remain higher-for-longer. Aurizon’s interest on drawn debt increased to 6.2% from 4.1% a year earlier.

Overall earnings guidance was cautious, leading analysts to trim their 2024-25 ASX200 earnings growth expectations to 3% (from 5%). This compares to about 17% forecast earnings growth for the US S&P500 Index.

The materials and financials sectors are most important for Australian investors, comprising about half of the market’s value.

Iron ore prices are the biggest driver of materials sector profits. They can be unpredictable, but they are expected to weaken further due to softer Chinese demand and increasing global supply. BHP’s recent results deck shows that a US$10/t change in the iron ore price impacts underlying earnings by about 8%, which is highly significant.

Australia’s major banks are an excellent example of where subdued profit growth hasn’t stopped share prices from rallying. CBA is the world’s most expensive listed bank, trading on about 23 times earnings compared to the global peer average of about 12 times.

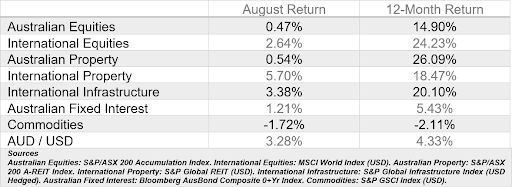

ASSET CLASS PERFORMANCE

You’re in! Thanks for subscribing.

Keep an eye on your inbox for exciting updates, offers, and news!

"*" indicates required fields