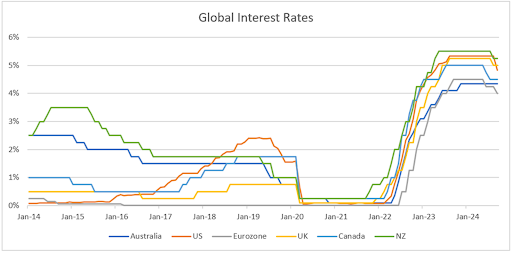

September was another eventful month for investors, highlighted by the US Federal Reserve’s first interest rate cut in over four years.

The other big news was the Chinese government’s announcement of a comprehensive stimulus package to stabilise the property market and bolster the economy. The barrage of easing measures covered many areas, including rate cuts, further relaxation of housing regulations (mortgages and downpayments), allowing companies to use the central bank’s funding to buy back shares and more support for buying unsold homes.

This is China’s largest stimulus since the pandemic and authorities have flagged that further stimulus would be forthcoming if necessary.

Such strong actions and messaging have us thinking back to 2012 when European Central Bank (ECB) President Mario Draghi promised to do “whatever it takes” to preserve the euro. This marked the turning point in the European sovereign debt crisis. Does Beijing share the same determination to support a full economic recovery?

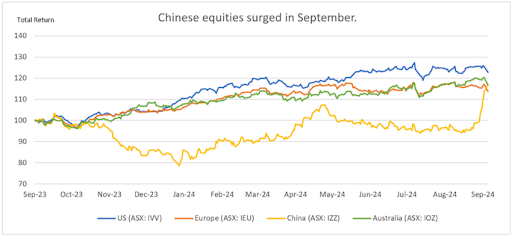

Investors seem to think so, driving Chinese equities +23% higher in September. Chinese equities have been trading on a low valuation of about 10x forward earnings compared to their global developed market counterparts (18x). This gap is now being narrowed as confidence in China’s economic outlook improves.

These developments once again highlight the advantages of portfolio diversification. Chinese equities typically have an approximate 25% weighting in Emerging Market ETFs such as the Vanguard FTSE Emerging Markets ETF (ASX: VGE).

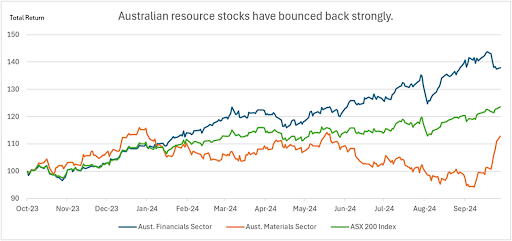

The actions taken by the US Fed and China support the global growth outlook and have provided a welcome boost to commodity prices. Australian resource equities are back in favor, while expensive banks have sold off.

We all know of the kicker to BHP, Rio Tinto and FMG’s profits from higher iron ore prices. Sustainably higher commodity prices would have broader positive implications for the Australian equity market and economy.

We note the recent comments made by ALS Limited (ASX: ALQ), a leading Australian analytical testing provider. The company has observed decreased activity in its geochemistry (assays) and metallurgy business. Lower assay demand reflects reduced exploration spending, stemming from challenges in raising capital due to negative investor sentiment.

Not even a sky-high gold price has been enough to revive the IPO market. In the first nine months of 2024, just 12 new resource/energy companies have hit the boards, well down from 25 in 2023 and 70 in 2022.

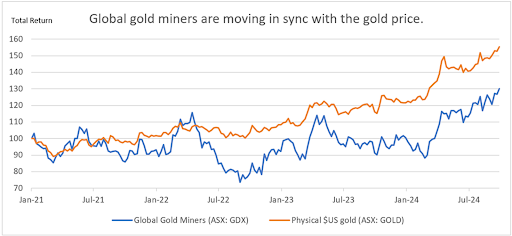

Gold continues to perform strongly, surpassing the US$2,600/oz mark for the first time in September. A lower US interest rate outlook (and a softer US dollar), escalating Middle Eastern conflict and uncertainty over the upcoming US Election have provided support.

Gold equities have yet to really take off, simply mirroring the movement in the price of the yellow metal.

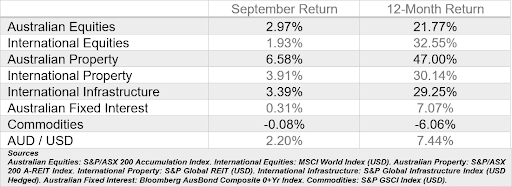

ASSET CLASS PERFORMANCE

You’re in! Thanks for subscribing.

Keep an eye on your inbox for exciting updates, offers, and news!

"*" indicates required fields