EXECUTIVE SUMMARY

- Australian equities hit record highs in February, led by gains in the financials and materials sectors.

- The earnings outlook is improving, with ASX 200 company profits expected to grow about 9% in FY26.

- The ASX 200 looks a bit pricey versus history – banks are fully valued, while resources appear fairly priced.

- Dividends remain an important part of total returns, even as yields have fallen with higher share prices.

- A wider range of ETFs is giving investors more options to diversify and target specific market areas.

BREAKING NEWS: MIDDLE EAST CONFLICT

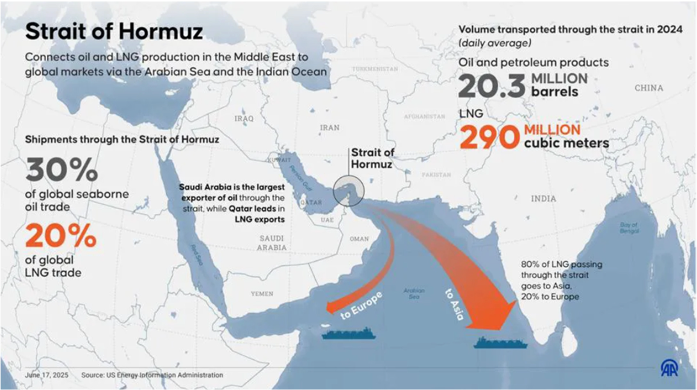

Conflict flared again in the Middle East in late February, following US and Israeli strikes on Iran. The situation remains highly uncertain, with many possible paths ahead.

For markets, the main issue is how long and how severely global shipping might be disrupted. This will affect growth and inflation expectations.

While Iran produces around 2% of the world’s oil, nearly 30% of global seaborne oil—and a similar share of global LNG—moves through the Strait of Hormuz, a key chokepoint in the region.

Any sustained blockage or slowdown there could affect energy supply and prices, especially for Asian (and European) economies that rely heavily on imported LNG.

MARKET SUMMARY

February was a strong month for global equity markets, with Australia, Europe and Japan all reaching record highs.

In Australia, attention focused on the reporting season as most leading companies released results, declared dividends and updated their outlooks.

Australian Earnings Season Summary

- It was a mixed reporting season, with about half of companies trading higher on the day of their announcements.

- The key Financials and Materials sectors, making up around 60% of the ASX 200, both performed strongly.

- The big four banks reported solid earnings supported by healthy credit growth, low bad debts and resilient profit margins.

- The major miners benefitted from higher production volumes and firmer commodity prices, particularly copper. Notably, BHP’s copper division generated more profit than its iron ore business for the first time.

- Aggregate ASX 200 earnings are on track to grow by around 9% in FY26, marking the first year of earnings growth in four years.

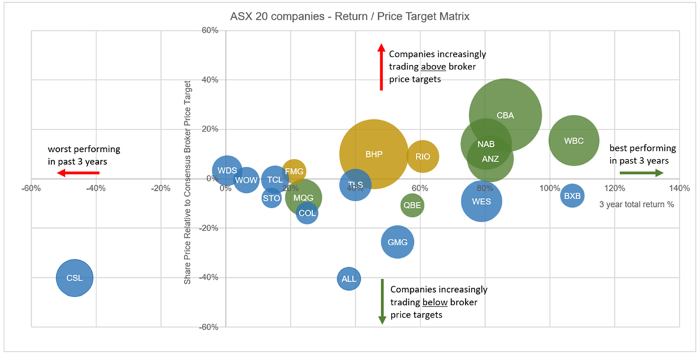

Have Share Prices Run Too Hard?

- With the market at record levels and uncertainty elevated (e.g. Middle East, Australian interest rates), some investors are starting to question whether the strong run can keep going.

- The chart below helps put this in perspective by plotting three-year total returns (x-axis) against consensus broker price targets (y-axis) for Australia’s 20 largest companies.

- The bubble size reflects each company’s weighting in the ASX 200.

- For example, Commonwealth Bank (CBA) – the index’s largest constituent – has returned +86% over the past 3 years and now trades about 26% above the average broker target price.

- Financials (shown as green bubbles) have led much of the market’s climb and their valuations now look stretched. The big four banks are trading on 20x forward earnings, compared with roughly 11x for their global peers.

- By contrast, the major resources companies (yellow bubbles) appear closer to fair value. Longer-term structural themes such as artificial intelligence, electrification and deglobalisation are contributing to a more supportive demand outlook for commodity-linked companies and potential earnings upside.

- Overall, the ASX 200 is currently trading on 17.1x forward earnings, versus a long-term average of 15.5x.

- In other words, investors are paying a premium for Australian equities today, but it is not extreme.

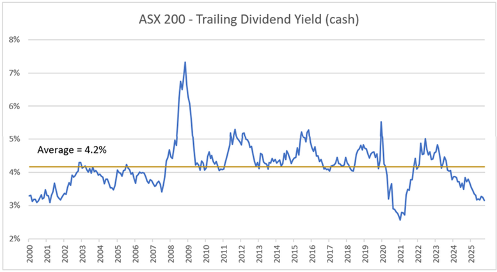

Dividend Yields Drifting Lower

- Australia is still attractive for equity income, but less so than in the past, as prices rise faster than dividends.

- The cash dividend yield on the ASX 200 is now about 3.2%, well below the 25-year average of 4.2%.

- Franking credits remain important, lifting the grossed-up yield to around 4.1%.

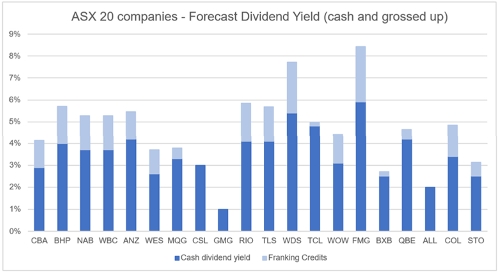

- Below are the forecast dividend yields currently available across ASX 20 companies.

More Choices with ETFs

With more Exchange Traded Funds (ETFs) now listed on the ASX, investors have greater flexibility to tailor their porfolios to their needs. Below, we outline a few options that may suit the current market environment.

Diversified Australian equity exposure

- Investors looking for broad Australian equity market —but with less concentration in the major banks and miners—might consider the VanEck Australian Equal Weight ETF (ASX: MVW).

- MVW holds an equal-weight portfolio of ASX-listed companies, increasing exposure to mid-caps and lifting allocations to sectors such as industrials and real estate.

Resources and energy exposure

- For those wanting to increase exposure to the resources and energy sectors, the VanEck Resources ETF (ASX: MVR) offers targeted access.

- Its holdings provide exposure to key commodities including iron ore, copper, gold, and oil and gas.

Income-focused equity options

- Several equity ETFs are designed specifically for higher income. Examples include the BetaShares S&P Australian Shares High Yield ETF (ASX: HYLD) and the Vanguard Australian Shares High Yield ETF (ASX: VHY), both of which currently offer forecast dividend yields of around 4–4.5% (plus franking).

- While these funds can enhance income, investors should note that they tend to hold more concentrated porfolios than broad market ETFs.

Other income opportunities

- With Australian interest rates expected to remain higher for longer in the short-medium term, investors may also benefit from lower-risk income sources.

- Cash and floating-rate bond ETFs can provide steady income with lower volatility than equities.

- Options include the BetaShares Australian High Interest Cash ETF (ASX: AAA), VanEck Australian Floating Rate ETF (ASX: FLOT) and iShares Yield Plus ETF (ASX: IYLD), which currently deliver income around 4–5%

- p.a. paid monthly.

MARKET UPDATE

US corporate earnings growth is broadening.

- It has been another solid quarter for US corporate earnings:

- According to FactSet, 73% of S&P 500 companies have beaten consensus expectations, with about 96% of the Index having reported so far.

- Aggregate earnings growth is running at 14.2% year-on-year, comfortably ahead of the 8.3%

- expected at the start of the season.

- The technology sector remains a standout performer, posting 33% earnings growth.

- Importantly, growth is now broadening beyond big tech.

- A useful gauge of this trend is the small-cap Russell 2000 Index – which tracks companies typically valued between US$250m to US$2 billion size and serves as a good barometer of the real economy.

- 65% of Russell 2000 companies have exceeded profit expectations, the highest level since mid-2021.

- Smaller businesses are rebounding as US interest rates decline, wage pressures ease and consumer spending stays resilient.

- The resilience of the American consumer also featured prominently in recent corporate commentary:

- Bank of America described the US consumer as “resilient and in great shape.”

- VISA and Mastercard both noted “continued healthy spending” across mass-market and affluent customer segments.

- Another positive sign for the broader economy is how technology investment is driving activity well beyond Silicon Valley. Caterpillar reported stronger profits thanks to rising demand for power-generation equipment used in AI data centres.

- This is a direct byproduct of surging big tech investment in AI and cloud infrastructure, which totaled roughly

- USD400 billion in 2026 and is projected to reach USD650 billion this year.

- Encouraging signs are emerging, but a sustained broadening of earnings growth is required to support a US equity market that continues to trade at a valuation premium.

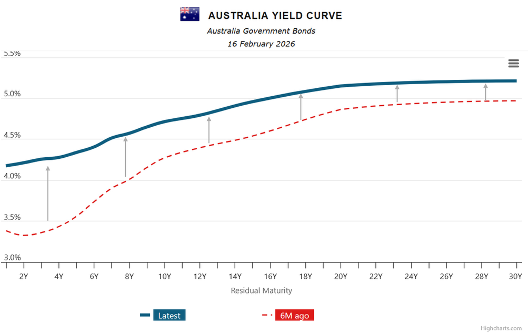

Fixed-rate bonds are investable again.

- In August last year, we reduced exposure to longer-duration bonds, anticipating that Australian inflation pressures could persist leading to higher bond yields and capital erosion.

- Our managed porfolios exited the BetaShares Australian Composite Bond ETF (ASX: OZBD), reallocating to the shorter-duration Vanguard Australian Corporate Fixed Interest ETF (ASX: VACF) and introducing the floating-rate Metrics Master Income Trust (ASX: MXT) across several porfolio types.

- That move proved well-judged. Markets have since shifted from expecting two 0.25% rate cuts (which never occurred) to pricing in two rate hikes, the first of which arrived in early February.

- Over the past six months, the Australian yield curve has shifted 0.40% to 0.90% higher, reflecting this “higher for longer” rate outlook.

- The good news is that today’s higher yields (lower prices) set a stronger foundation for 2026 fixed-income returns.

- We’re now comfortable reintroducing a measured level of longer term-duration exposure into defensive allocations.

- Our preferred high-quality longer-duration Australian bond ETFs include:

- BetaShares Australian Composite Bond ETF (ASX: OZBD) – approximately 5.5 years duration

- Coolabah Active Composite Bond ETF (ASX: FIXD) – approximately 4.9 years duration

- For additional diversification, we continue to favour the VanEck Emerging Income Opportunities Active ETF (ASX: EBND). It invests in a diversified porfolio of emerging market bonds and currently carries a 6.1-year duration.

ASSET CLASS PERFORMANCE

Australian Equities

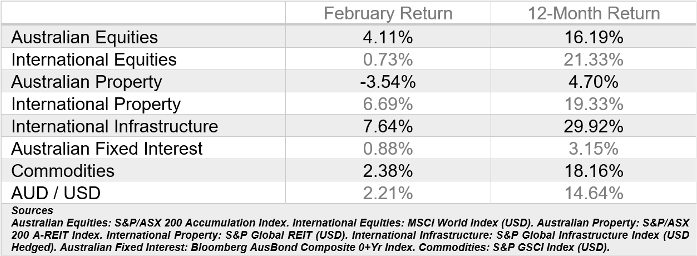

- The Australian equity market had a strong February, with the S&P/ASX 200 Index rising +4.1% for the month.

- Financials (+9.2%) and Materials (+9.1%) led the way, supported by solid earnings results from major banks and resources companies.

- Shares in Westpac, National Australia Bank, ANZ Group and BHP Group shares all reached record highs during the month.

- At the other end of the spectrum, the Healthcare sector slid -13.3%, dragged down by a -19.1% decline in CSL after its first half earnings disappointed investors. However, better results from Sonic Healthcare and Ramsay Health Care helped limit the sector’s overall decline.

- The Technology sector also remained under pressure, losing a further -9.4% in February and is now down -43% from its peak six months ago.

International Equities

- Global equities extended their winning streak to an eleventh straight month in February, with the MSCI All-World Index rising +0.7%. Most of the strength came from markets outside the US.

- Japanese equities jumped +9.3% after Prime Minister Sanae Takaichi’s decisive election victory boosted confidence in further fiscal stimulus.

- European markets also performed well, up +3.4%, supported by a stronger corporate earnings outlook and record levels of share buybacks. February marked Europe’s eighth consecutive month of gains – its longest winning run since 2012-2013.

- In contrast, US technology stocks lagged, with the Nasdaq falling -3.3%. Investors showed growing caution toward large tech firms, questioning whether their significant spending will deliver the revenue growth expected. Concerns also rose for some software companies that may face disruption from rapid advances in artificial intelligence.

- Emerging markets lifted +2.4%, buoyed by strength in Taiwan, which helped offset weaker performance in China and India.

Property and Infrastructure

- Global listed global infrastructure and property were among the strongest performers in February, rising +7.6% and +6.7% respectively.

- These sectors benefitted from a more moderate global interest rate outlook, resilience and growing income streams and rising investor demand for real assets.

- In contrast, Australian Property lagged behind, falling -3.5% reflecting the higher for longer Australian interest rate outlook.

Fixed Income

- The Bloomberg Australian Bond Index rose +0.88% in February.

- Early in the month, the Reserve Bank of Australia lifted the cash rate by 0.25% and indicated that additional increases may still be needed to contain inflation.

- Financial markets have now fully priced in another 0.25% rate rise by August 2026.